CMA part2 شرح سامح الليثي 11

.

نستعين بالله ونكمل قصة الCosting and Pricing for the Long Run ولسع شغالين في الmarket-based approach

.

ومعادنا مع ال5 خطوات بتوع ال target prices and target costs

.

عايزين نعرف لو انا النهاردة حبينا نعمل Implementing للTarget Pricing and Target Costing ايه اللي الشركة محتاجة تعمله؟؟

.

في الحقيقة هورنجرين جايبلك five steps in developing target prices and target costs. وعشان الدنيا توضح استخدم Provalue example

.

الخطوات طبعا لابد انها تكون متسقة لخل الmarket-based approach فبدات فعلا بالعميل وبعدها السعر في الخطوة التانية راحت في الخطوة التالتة هنشوف الادارة نفسها تكسب كام

يبقى سعر ناقص ربح يديني التكلفة المستهدفة ونحللها ونعمل الvalue engineering

.

طيب الخطوات الخمسة مهمين جدا كامتحان cma لانك لو تعبت نفسك شوية وروحت على الLearning Outcome Statements

.

هتلاقي 4 نقاط كالتالي:

g. identify techniques used to set prices based on understanding customers’ perceptions of value, competitors’ technologies, products and costs

h. define and demonstrate an understanding of target pricing and target costing and identify the main steps in developing target prices and target costs

i. define value engineering

.

فسيادتك الخمس خطوات اللي جايين دول يبقوا زي اسمك

.

هنقولهم كعناوين ونعملهم اختصار يفكرنا بيهم لو جم في الessay وبعدها نشرحهم إن شاء الله

.

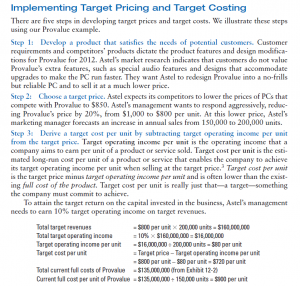

Step 1: Develop a product that satisfies the needs of potential customers.

.

بدايتنا نشوف العميل ايه المنتج اللي يرضيه (ندي الخطوة دي حرف الc بتاع الcustomers)

.

Step 2: Choose a target price.

.

نشوف المنافسين ونشوف ايه السعر الافضل لطرح المنتج (ندي الخطوة دي حرف الp بتاع الprice.)

.

Step 3: Derive a target cost per unit by subtracting target operating income per unit

from the target price.

.

ببساطة هناخد السعر نطرحه من الربح اللي نفسنا فيه هنطلع بالtarget cost (ندي الخطوة دي حرف الc بتاع الcost .)

.

Step 4: Perform cost analysis

.

تحليل التكلفة (ندي الخطوة دي حرف الa بتاع الanalysis)

.

Step 5: Perform value engineering to achieve target cost.

.

(ندي الخطوة دي حرف الv بتاع الvalue )

.

يبقى اختصارها: CP-CAV

.

…………….*******************………….

.

زي ما انت شايف هورنجرين استخدم مثال الProvalue

.

طيب افكرك سريعا المعلومات اللي كانت تخص الProvalue ده في 2011 لكمية وحدات عاملة 150 الف وحدة كان السعر 1000 دولار ولو فاك كانت الmanufacturing cost للوحدة كانت عاملة 680 دولار منهم لو تفتكر 600 تكلفة مباشرة و80 غير مباشرة

.

وفوق التكاليف الصناعية عندنا 220 دولار حبة Operating costs فيدينا اجمالي Full cost of the product عاملة 900 دولار فكان الOperating income للوحدة 100 دولار

.

المهم هورنجرين بيقولك ان Step 1: في الTarget Pricing هي

.

Develop a product that satisfies the needs of potential customers.

.

طبعا العميل والمنافس هم شغلنا الشاغل في الخطوة دي عشان كدة بنقول:

Customer requirements and competitors’ products dictate the product features and design modifications

for Provalue for 2012.

.

الغريب ان البحوث التسويقية بتاعت شركة Astel اكتشفت ان العميل مش بيقدر Provalue’s extra features زي مثلا

.

Astel’s market research indicates that customers do not value

Provalue’s extra features, such as special audio features and designs that accommodate

upgrades to make the PC run faster.

.

يعني الزباين نفسهم ان Astel تعيد تصميم الProvalue ومن الاخر يكون بسعر اقل

.

They want Astel to redesign Provalue into a no-frills

but reliable PC and to sell it at a much lower price.

.

………***********………

.

بعد اما عرفنا العميل عايز ايه هنخش على Step 2: Choose a target price.

.

Astel expects its competitors to lower the prices of PCs that

compete with Provalue to $850.

.

فالشركة قالت لا طب انا هنزله بخصم 20% عن سعره يعني يعمل بدل 1000 دولار يبقى ب800 دولار

.

Astel’s management wants to respond aggressively, reducing

Provalue’s price by 20%, from $1,000 to $800 per unit.

.

وكقوانين اقتصاد طالما السعر قل يبقى نتوقع ال150 الف وحدة يزيدوا وفعلا الشركة متنبأة انها تبقى ل200 الف وحدة

At this lower price, Astel’s

marketing manager forecasts an increase in annual sales from 150,000 to 200,000 units.

.

………………*****************………..

.

بعد اما السعر ابو 800 دولار بقى في ايدينا نخش على Step 3:ونحاول نعرف الtarget cost per unit في ظل تطلعات الادراة لربح معين اهو هنمسك السعر ابو 800 ده ونطرح اللي الادارة عايزه

.

Step 3: Derive a target cost per unit by subtracting target operating income per unit

from the target price.

.

وبساطة الTarget operating income per unit هو operating income that a

company aims to earn per unit of a product or service sold

.

وعليه التكلفة المستهدفة هي التكلفة المقدرة في الاجل الطويل اللي هتخلينا نحقق الtarget operating income per unit أما تبيع عند السعر اللي قلنا عليه

.

Target cost per unit is the estimated

long-run cost per unit of a product or service that enables the company to achieve

its target operating income per unit when selling at the target price.

.

.

من الكلمتين دول بقى عملوا المعادلة بتاعت التكلفة مستهدفة اللي هوك لسه كان قايلهانا

.

Target Price – Target Operating Income Per Unit = Target Cost Per Unit

.

بص على المعادلة كويس

.

وشوف هورنجرين بيقولك ايه:

.

Target cost per unit

is the target price minus target operating income per unit

.

وفعلا دي المعادلة بالظبط بس هورنجرين بيلفت انتباهك انه:

.

and is often lower than the existing

full cost of the product.

.

لو تفتكر من تحليل تكلفة ال Provalue كان تكلفته عاملة 900 دولار

.

المهم تحط في دماغك:

.

Target cost per unit is really just that—a target—something

the company must commit to achieve.

.

روحنا لادارة الشركة وسئلنها انت حط في دماغك عائد كام؟

.

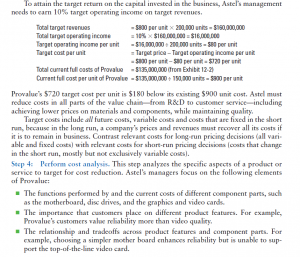

To attain the target return on the capital invested in the business, Astel’s management

needs to earn 10% target operating income on target revenues.

.

طيب بتخفيض السعر احنا بنتكلم في

Total target revenues عامل 160 مليون من خلال بيع ال200 الف وحدة على السعر الجديد ابو 800 دولار

.

والادارة نفسها في Total target operating income عامل 10% يعني 16 مليون

.

يعني كل وحدة تكسب 80 دولار

.

والسعر عامل 800 دولار يبقى يا باشا الTarget cost per unit لازم تبقى 720 دولار

.

وانت كنت بتتكلم لو فاكر عند مستوى ال150 الف وحدة في تكلفة full costs of Provalue عامل 900 دولار

.

ياااااااااااااه ده احنا محتاجين نخفض حوالي 180 دولار

.

Provalue’s $720 target cost per unit is $180 below its existing $900 unit cost.

.

طيب وازاي؟؟ خفض تكاليف بس حافظ على الجودة

.

Astel must reduce costs in all parts of the value chain—from R&D to customer service—including

achieving lower prices on materials and components, while maintaining quality.

.

.

وزي ما قلنا :

.

Target costs include all future costs, variable costs and costs that are fixed in the short

run, because in the long run, a company’s prices and revenues must recover all its costs if

it is to remain in business.

.

بس هورنجرين بيقولك لازم تكون اخد بالك بالفرق بين الrelevant costs في الاجل الطويل (اللي هي كل التكاليف بغض النظر عن سلوكها) مع التكاليف الrelevant في الاجل القصير (اللي معظمها هتلاقيه متغيرة)

.

Contrast relevant costs for long-run pricing decisions (all variable

and fixed costs) with relevant costs for short-run pricing decisions (costs that change

in the short run, mostly but not exclusively variable costs).

.

خلاص من Step 3 بقى في ايدينا ال720 الtarget cost هنحتاج بقى نشوف ازاي هنوصلها وهنخفض حوالي 180 دولار وده هيلزمن اننا نعمل تحليل للتكلفة

.

Step 4: Perform cost analysis.

.

This step analyzes the specific aspects of a product or

service to target for cost reduction.

.

خلاص من الممكن تصور ان Astel’s managers هيركزوا على عناصر معينة للProvalue زي

..

مثلا يروح يشوف الcomponent parts بتاعت الProvalue شغالة ازاي وتكلفتها كام مثلا الmotherboard وdisc drives وهكذا

.

The functions performed by and the current costs of different component parts, such

as the motherboard, disc drives, and the graphics and video cards.

.

مثلا يروح يشوف الزباين بيميلوا اكتر لايه بيقدروا ايه مثلا هل value reliability more than video quality ؟؟

.

The importance that customers place on different product features. For example,

Provalue’s customers value reliability more than video quality.

.

يعملوا موازنة بين الfeatures بتاعت المكونات زي الreliability في ظل اختيار simpler mother board بس مش هتدي الزبون top-of-the-line video card

.

The relationship and tradeoffs across product features and component parts. For

example, choosing a simpler mother board enhances reliability but is unable to support

the top-of-the-line video card.

.

.

بعد الهري بتاع التحليل ده المصممين والمهندسي عليهم عبء اداء الvalue engineering اللي يوصلنا لل720 دولار دي ويخفض ال180 دولار

.

Step 5: Perform value engineering to achieve target cost.

.

وخده كلمة لو حد سئلك ايه الvalue engineering ده ؟؟

.

لازم اجابتك تبقى واضحة اولا هو systematic evaluation ؟؟ يعني تقييم منظم

.

لايه ؟؟؟

.

لكل جوانب سلسلة القيمة

of all aspects of the value chain

.

عشان خاطر ايه؟؟؟ حاجتين تخفيض تكاليف وفي نفس الوقت تحقيق الجودة اللي ترضي الزبون

.

with the objective of reducing costs and

achieving a quality level that satisfies customers.

.

ودي نتصور فيها ايه؟؟ طبعا ممكن نضطر نحسن تصميم المنتج ونغير مثلا المادة الخام وطريقة الانتاج وهكذا

.

improvements in product designs

.

changes in materials specifications

.

modifications in process methods.

.

….

.

طبعا لو حبيت تشوف مثال جيد للtarget pricing and target costing مش هتلاقي احسن من ايكيا هنرفها لزيادة المدارك وللاطلاع بس

.

…………..

.

طيب بص بقلى البوست ده غطى نقطتين من الLOS مهمين جدا خصوصا للايساي

.

الاولى النقطة H

.

h. define and demonstrate an understanding of target pricing and target costing and identify the main steps in developing target prices and target costs

.

والنقطة I

.

i. define value engineering

.

طيب محتاجين نخش على النقطة اللي بعد كدة ازاي

.

calculate the target operating income per unit and target cost per unit

.

j. calculate the target operating income per unit and target cost per unit

k. define and distinguish between a value-added cost and a nonvalue-added cost

.

ودول من خلال البوستين اللي جايين ان شاء الله

.

طيب نوقف البوست على كدة ونخش على اللي اتفقنا عليه يسر الله الأمر وأعان

زر الذهاب إلى الأعلى