CMA part2 شرح سامح الليثي 12

نستعين بالله ونحاول من خلال البوست ده نغطي جزئية في الLOS مرتبطة بالvalue engineering والتمييز بين الa value-added cost and a nonvalue-added cost

.

واحنا اخر حاجة كنا واقفين على عنوان Value Engineering, Cost Incurrence, and

Locked-In Costs

.

Value Engineering اللي بيسموها هندسة القيمة اللي بتعمل زي ما قلنا تقييم منظم لسلسلة القيمة عشان نخفض التكلفة ونرضي العميل بجودة كويسة

.

بس هورنجرين حاطط في العنوان Cost Incurrence يعني حدوث التكلفة

.

وحاطط Locked-In Costs اللي بيسموها التكاليف المقررة أو المحددة سلفا أو احيانا بنقول عليها المصممة designed in,

.

بص يا سيدي

.

اصلا عشان خاطر To implement value engineering لازم المديرين يا باشا

.

managers distinguish value-added activities and costs

from nonvalue-added activities and costs.

.

وبديهيا التكلفة اللي بتضيف قيمة لو شيلناها القيمة اللي شايفها العميل في منتجنا هتقل

.

A value-added cost is a cost that, if eliminated,

would reduce the actual or perceived value or utility (usefulness) customers experience

from using the product or service.

.

ودي طبعا زي التكاليف بتاعت تحيقي الreliability, ومثلا ذاكرة ككافية في الكمبيوتر الخ

.

Examples are costs of specific product features and

attributes desired by customers, such as reliability, adequate memory, preloaded software,

clear images, and, in the case of Provalue, prompt customer service.

.

على الناحية التانية هنلاقي الA nonvalue-added cost is a cost that,

.

بص بقى

if eliminated, would not reduce the actual or

perceived value or utility (usefulness) customers gain from using the product or service.

.

اللي من الاخر الزبون مش عايز يدفع فيها مليم

It

is a cost that the customer is unwilling to pay for

.

زي مثلا التكاليف بتاعت اعادة تشغيل واصلاح المنتجات البايظة

.

Examples of nonvalue-added costs are

costs of producing defective products and cost of machine breakdowns.

.

وطبعا الSuccessful companies

keep nonvalue-added costs to a minimum.

.

واحد يقول minimum. ليه احنا عايزين نلغيها خالص!!

.

نقول له اصبر القصة مش بالسهولة والوضوح ده للاسف هتلاقي

Activities and their costs do not always fall neatly into value-added or nonvalueadded

categories.

.

يعني في منطقة رمادية زي مثلا الاشراف والتحكم في الانتاج جوة الانشطة دي هتلاقي حبة بيضيفوا وحبة مش اوي

.

Some costs, such as supervision and production control, fall in a gray

area because they include mostly value-added but also some nonvalue-added components.

.

بس عامة:

Despite these troublesome gray areas, attempts to distinguish value-added from nonvalueadded

costs provide a useful overall framework for value engineering.

.

عارف لو رجعنا لProvalue example هتلاقي كل التكاليف المباشرة بتضيف قيمة

In the Provalue example, direct materials, direct manufacturing labor, and direct

machining costs are value-added costs.

.

الا ان كلا من اوامر الشراء والاستلام والفحص دي رمادية اللون

Ordering, receiving, testing, and inspection costs

fall in the gray area.

.

لكن مثلا الRework costs are nonvalue-added costs.

.

.

طبعا في المتوقع انه يحصل حاجتين:

.

Through value engineering, Astel’s managers plan to reduce, and possibly eliminate,

nonvalue-added costs

.

دي رقم واحد

.

وكمان

and increase the efficiency of value-added activities.

ودي رقم اتنين

.

وهنا بقى هنبتدي نفرق بين التكاليف المقررة و Cost Incurrence حدوث التكلفة …

.

They start by

distinguishing cost incurrence from locked-in costs.

.

واحد يقول لي معلش ايه قصة الCost Incurrence؟؟

.

نقول له دي محاسبة التكاليف حضرتك بتاعت بارت وان التكلفة بتاعت الكرسي اللي مثلا الJOB ORDER حسبها

.

Cost incurrence describes when a

resource is consumed (or benefit forgone) to meet a specific objective.

.

Costing systems

measure cost incurrence.

.

وتطبيقها على مثالنا هنا انه مبجرد صنعت Provalue هتصرف مادة خام مع كل وحدة بتصنعها

.

Astel, for example, recognizes direct material costs of Provalue

as each unit of Provalue is assembled and sold.

.

لكن الجديد هنا ان اصلا في مرحلة مبكرة في تصميم الProvalue يوم اما المصممين اختارو المكونات اللي هيسخدموها في التصنيع

.

But Provalue’s direct material cost per unit

is locked in, or designed in, much earlier, when product designers choose Provalue’s components.

.

عشان كدة بنقولك:

.

Locked-in costs, or designed-in costs, are costs that have not yet been incurred

but,

.

اخد بالك لسه محصلتش لكن بناء على قرار اختيارها في التصميم هتحصل

.

but, based on decisions that have already been made, will be incurred in the future.

.

يبقى خلاص بديهيا To manage costs well, هنعمل ايه بقى؟؟ الشركة محتاجة تعرف ايه من التكاليف في مرحلة التصميم هيربط بتكلفة معينة

.

a company must identify how design choices lock in costs

before the costs are incurred.

.

ومثاله تكلفة الخردة اللي هتظهرلك بسبب مشاكل في تصميم المنتج سيادتك:

.

For example, scrap and rework costs incurred during manufacturing

are often locked in much earlier by faulty design.

.

وعند شركات البرامج حتة الerrors اللي هتظهر في مرحلة الcoding بسبب مشاكل في تصميم السوفتوير اصلا

.

Similarly, in the software

industry, costly and difficult-to-fix errors that appear during coding and testing are frequently

locked in by bad software design and analysis.

.

.

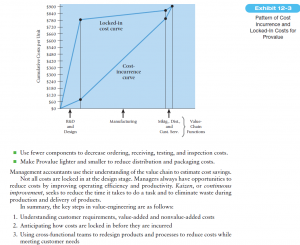

هورنجرين بيقولكهو انت مش ملاحظ انك اما بتصرف في R &D costs (كنا قايلين دولار36 ) وفي الDesign حوالي 40 دولار يعني معانا وانت صارف حوالي 8% من التكلفة سيادتك بتورطنا في حوالي 780 دولار تكاليف صناعية وتسويقية بقرارات التصميم اللي كلفتنا بس 76 دولار:

.

Observe, however, the wide divergence between when costs are locked in and when they

are incurred. For example, product design decisions lock in more than 86% ($780 ÷

$900) of the unit cost of Provalue (for example, direct materials, ordering, testing,

rework, distribution, and customer service), when only about 8% ($76 ÷ $900) of the

unit cost is actually incurred!

.

…………*********……….

.

طيب هنعمل ايه بقى عشان نخفض التكاليف؟؟

.

هنكون cross-functional value-engineering team

.

من ادارات كتير من :

.

marketing managers, product

designers, manufacturing engineers, purchasing managers, suppliers, dealers,

.

وطبعا الmanagement

accountants

.

عشان edesign Provalue to reduce costs while retaining features that customers

value.

.

ممكن مثلا نتصور افكار زي Use a simpler, more-reliable motherboard without complex features تخفض التكاليف الصناعية والاصلاح

.

تسهل الاجزاء بتاعته شوية قتقلل ساعات العمالة

.

Snap-fit rather than solder parts together to decrease direct manufacturing laborhours

and related costs.

.

Use fewer components عشان نقلل ordering, receiving, testing, and inspection costs

.

نخلي الProvalue يبقى lighter and smaller عشان نقلل distribution and packaging costs

.

طبعا حبايبنا الManagement accountants لازم use their understanding of the value chain to estimate cost savings

.

لانه طبعا :

.

Not all costs are locked in at the design stage.

.

فإن شاء الله في أمل:

.

Managers always have opportunities to

reduce costs by improving operating efficiency and productivity.

.

وزي ما قلنا في بارت وان

Kaizen, or continuous

improvement, seeks to reduce the time it takes to do a task and to eliminate waste during

production and delivery of products.

.

طيب عايزين نقولك In summary الthe key steps in value-engineering اللي ممكن سيادتك تكتبها في الESSAY لو اتسئلت عليها:

.

افهم لي الزبون عايز ايه وايه من التكاليف بيضفلو قيمة وايه مش بيضيف

Understanding customer requirements, value-added and nonvalue-added costs

.

وعينك في وسط راسك ايه من التكاليف هتبقى locked من مرحلة التصميم

Anticipating how costs are locked in before they are incurred

.

واخيرا فريق العمل اللي هيشوف ازاي يخفض التكلفة

.

Using cross-functional teams to redesign products and processes to reduce costs while

meeting customer needs

.

طيب محتاجين بقى نحقق ال720 دولار الTarget Cost بتاعت الProvalue بس دي نخليها في البوست اللي جاي يسر الله الأمر وأعان

زر الذهاب إلى الأعلى