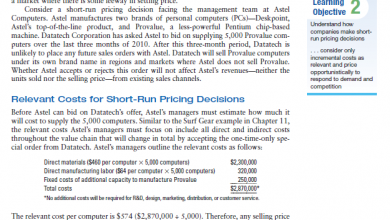

CMA 2020 شرح سامح الليثي النظام الجديد 8-11

CMA 2020 شرح سامح الليثي النظام الجديد 8-11

تاني بوست لشرح للIntegrated reporting

.

نستعين بالله عزوجل ونكمل الكلام على الIntegrated reporting ونحاول نعرف ايه المقصود به واللي مطلوب في الجزئية دي في الlos

.

هوك بعد أما عمل مقدمة زي ما شوفنا في البوست اللي فات ووضح ايه اصلا الNon-financial Information وليه بنعمل لها تقرير

.

عمل عنوان تاني اسمه:

.

The Movement to Report Non-Financial Information

.

وقالك الكلمتين اللي نبهنا عليهم ان الmovement to report on non-financial information بدأت فعليا في 1950s to early 1960s

.

ليه؟؟

.

استجابة زي ما قلنا لneeds of information users

.

اللي بعد كدة سميناهم “stakeholders,”

.

وطيب ليه بردو؟؟

.

عشان وركز اوي على الكلمة دي:

.

لتقديم مؤكد information بس beyond what was

presented in financial statements

.

عشان خاطر نوضح بشكل افضل الvalue-creation process بتاع الشركة وكمان المخاطر بتاعتها الغير مالية.

.

وزي ما قلنا ان ال“stakeholders,” دول يعتبروا الاطراف اللي ليهم مصلحة مع الشركة سواء او اللي بيتأثروا بأفعال الشركة

.

سواء الemployees, او الmanagers, owners, customers, suppliers, society, government, and creditors.

.

الفكرة بتاعت انهم بيغنوا على اضافة قيمة لل“stakeholders,” بمعنى ان جذر الموضوع ده انهم جم قالولك طبقا للstakeholder theory

.

لازم شغل الشركة يتفهم كنظام بيضيف قيمة لل“stakeholders,”

.

فاكر زمان كنا بنقعد ندندن على ان الشركة تضيف قيمة للshareholders.

.

وان الهدف الرئيسي انها ت

corporation’s sole responsibility is to maximize value for its shareholders

.

جم هنا قالولك لأ بص بقى الstakeholder theory دي بقى contrast مع موضوع ان الcorporation’s sole responsibility يكون للmaximize value for its shareholders

.

ورفعوا شعار

.

The stakeholder

worldview connects business and capitalism with ethics

.

يا سلام……

.

.

ومع مرور السنين مفهومين منفصلين بس بيكملوا بعض اندمجوا بقى

.

مفهوم عشان خاطر يبين اثر الشركة على المجتمع وده اسمه: “corporate social responsibility”

.

والمفهوم التاني بتاع التنمية اللي تبقى على طول: “sustainable development.” اللي بيركز على ان الشركة بتلبي الاحتياجات بتاعت النهاردة بس دون المساس بقدرة الأجيال المقبلة على تلبية احتياجاتهم

.

يعني بالبلدي اه ت

focuses on organizations’ meeting the

needs of the present

.

بس مش بس

.

من غير:

.

without compromising the ability of future generations to meet their own needs

.

.

طبعا طلعوا على 2010 بايزو للSocial Responsibility رقم 26 الف قالك انا هساعد الشركات تحط هيكل للsr

.

وتقيمها وتطورها كمان متضمنا their stakeholder relationships and community impacts

.

والميزة ان الايزو ده حدد الsociety’s expectations عن ايه اللي بيمثل socially responsible behavior فالشركات تحطه كbenchmark ليها

.

انت حتى لو بصيت هتلاقي ان تعريف social responsibility اللي الايزو حطوه مخل الsustainable development تحت الumbrella اصلا بتاعت الsr

.

حتى يقولك ايه الsr هي مسؤلية الشركة عن تأثير قرارتها وانشطتها على المجتمع والبيئة بس من خلال transparent and ethical behavior

.

اللي -بص بقى ازاي هيدخل حة الsustainable development –

.

بيقولك عايزين سلوك منك يا شركة يكون transparent and ethical عشان

.

واحد:

.

يا شركة ساهمي في sustainable development

.

1) Contributes to sustainable development, including the health and welfare of society,

.

تاني نقطة

.

روحي شوفي ايه الexpectations بتاعت الstakeholders,

.

2) Takes into account the expectations of stakeholders,

.

تالت نقطة:

.

3) Complies with applicable law and is consistent with international norms of behavior, and

.

رابع نقطة:

.

4) Is integrated throughout the organization and practiced in its relationships.

.

بس اللي تلاحظه ان الايزو ده زي ما انت شايف قدم ارشاد ازاي الشركات تبقى socially responsible لكن مقدمش للاسف اطار لreporting on social responsibility

.

بس على الناحية التانية في منظمة كدة غير حكومية كانت قدمت اطار للreporting بتاع الsocial responsibility and sustainable development activities

.

الاطار ده اسمه الGlobal Reporting Initiative (GRI). بيعتبروا الinternational standard بتاع

.

reporting on environmental and social

responsibility, including sustainability, and economic performance.

.

طيب نوقف البوست ده على كدة ونخش من البوست اللي جاي على Reporting Requirements عشان نجاوب على سؤال مهم اوي هل في mandatory requirements للتقرير عن البيانات ال non-financial ؟؟

.

يسر الله الأمر وأعان

.

تالت بوست لشرح للIntegrated reporting

.

نستعين بالله عزوجل ونكمل الكلام على الIntegrated reporting

.

معادنا مع ال Reporting Requirements عشان نجاوب على سؤال مهم اوي هل في mandatory requirements للتقرير عن البيانات ال non-financial ؟؟

.

بص يا سيدي

.

لو مشيناها بالدول هتلاقي الاتي:

.

The U.S. has no mandatory non-financial reporting requirements other than some required disclosures

about mine safety and conflict minerals.

.

بس خلي بالك:

.

However, many of the largest U.S. companies prepare non-financial

reports on a voluntary basis.

.

طيب نطلع برة الU.S. هتلاقي حاجة غريبة اوي

.

Many countries outside the U.S. have mandatory non-financial reporting requirements

.

طيب امثلة سريعة:

.

In 2014, the European Commission issued a Directive (Directive 2014/95/EU) on disclosure of non-financial

and diversity information by large, public-interest entities (listed companies, banks, insurance companies,

and other companies designated as such by authoritative bodies) and generally having more than 500

employees.

.

اهو الDirective ده لازم اي EU-member country تطبقه

.

بس يكون:

.

into its own legislative requirements,

though member countries were allowed some flexibility in adapting the terms.

.

طيب ايه بقى اللي مطلوب من الCovered EU companies ؟؟

.

اولا:

.

Covered EU companies are required to report on policies, risks, and program outcomes related to environmental

protection, social responsibility, treatment of employees, respect for human rights, and

anticorruption and bribery matters.

.

وهتلاقي ان الCompanies licensed to trade securities بردو لازم يطلعو

.

a diversity report

containing information about age, gender,

and professional and educational backgrounds at different management

levels.

.

.

طيب الNon-financial statements دي هنعرضها ازاي؟؟

.

قالك ممكن

may be presented to stakeholders either in the company’s annual

report

.

او

as a separate report published alongside the annual report or within six months of the balance

sheet date.

.

.

وهنا ال

بتاعت الDirective طالب اصلا ان الstatutory auditor تعمل تأكيد ان الrequired nonfinancial

disclosures have been published

.

بس مش طالبة انه يراجع محتوياتها.

.

*******

.

لو روحنا على South Africa هتلاقيها انها اول دولة اصلا تدخل الintegrated reporting من ضمن الofficial reporting requirements

.

.

ومطلعين Code of Governance بيقولك:

.

“the board should appreciate that

strategy, risk, performance, and sustainability are inseparable”

.

المهم انه بيوصي كمان الشركات انها تعمل :

integrated report including non-financial information along with financial information

.

بس الامر كمان وصل ان الكلام ده خلوه من ضمن الlisting requirements بتاعت البورصة هناك

.

وعليه:

listed companies are required to prepare an integrated report or explain why they are not doing so.

.

بعدها بقى طلع Integrated Reporting Committee (IRC) of South Africa

عمل تجميعة حلوة كدة ل

accountants, companies, internal

auditors, directors, institutional investors, the JSE, and others with an interest in corporate reporting.

.

.

وعمل الاطار بتاع الintegrated report in 2011

.

والاطار ده كان نقطة البداية ل

development of the International Integrated Reporting Council’s (IIRC) International

<IR> Framework, which was issued in 2013.

.

.

عشان كدة جليم جمع الكلام ده في سطرين حلوين وقالك تلاحظ من الكلام ان الIntegrated reporting is a relatively new concept

.

وبدأنا نحس بانتشاره خصوصا اما اتعمل الInternational Integrated

Reporting Council (IIRC) in 2010.

.

وزي ما هوك لسه قايل جليم بيعلق :

.

This global entity, composed of regulators, organizations, accounting firms, and

standards setters, issued the International <IR> (Integrated Reporting) Framework in 2013.

.

بس زود كلمة جميلة اوي:

.

The objective is to bring together capital allocation

and corporate activity to create financial well-being and sustainable expansion through the use of integrated thinking and

integrated reporting.

.

بيقولك الهدف اننا نضم مع بعض كلا من capital allocation مع الcorporate activity عشان نخلق financial well-being and sustainable expansion من خلال

.

integrated thinking and integrated reporting. زي ما هنشوف في البوستات الجاية

.

وقفل كلامه في الحتة دي بكلمة فيها أمل لتوسيع نطاق الIR فبيقولك:

.

Although the <IR> Framework primarily focuses on providers of financial capital in the private sector, its mission is for IR to

become the worldwide corporate reporting standard for both private and public companies.

.

.

بس يا سيدي دي قصة الReporting Requirements هنوقف على كدة في البوست ده لاننا محتاجين نتكلم شوية على الInternational <IR> Framework نفسه

.

نستعين بالله ونتكلم شوية عن The International <IR> Framework اللي قدمه المجلس الدولي بتاع الIR على اغسطس 2010

.

طبعا جمعوا ناس من كذا حتة مع بعض

.

bringing together a cross-section of representatives from the corporate, investment,

accounting, securities, regulatory, academic, and standard-setting sectors as well as civil society.

.

وقالوا احنا الغرض بتاعنا اننا نعمل globally-accepted framework للprocess اللي تخلي الشركات توصل بيها جهودها تجاه الvalue creation over time.

.

وكان نتاج شغلهم الInternational <IR> Framework اللي طلع في 2013

.

لو فتحت النهاردة الwebsite بتاع الIIRC هتلاقي طبعا اندماج global

للregulators, investors, companies, standard setters,

the accounting profession, and non-governmental organizations

(NGOs).

.

الcoalition والاندماج ده بيعمل promotes لحتة الcommunication about value creation

.

طبعا حتة خلق القيمة دي تم توضيحها في البوستات اللي فاتت الا ان الCouncil بتاع الIIR عملها تعريف داخل الاطار وقالك بصو يا جماعة احنا نقصد بالValue creation

.

انها العملية اللي هينتج عنها زيادة او تخفيض او حتى نقل للcapitals (طبعا يقصدو بالcapitals الموارد بتاعت الشركة اللي بتستخدم للانتاج السلع او تقديم الخدمات)

.

المهم قلنا انها العملية اللي هينتج عنها زيادة او تخفيض او حتى نقل للcapitals التي تسببت فيها أنشطة الشركة ومخرجاتها.

.

يعني لو انت مساهم والشركة بتبيع كراسي وبتكسب هتلاقي موارد الشركة بتزيد….ده المعنى في ابسط صوره.

.

حتى ويلي بيقولك:

In short, value creation is the sum of the organization’s activities which,

in theory, aims to increase the overall stock of capitals.

.

.For example, an organization’s financial capital is increased when it makes a profit,

and the quality of its human capital is improved when employees become better trained.

.

طبعا الCouncil بتاع الIIR عمل لنفسه mission يأسس بيها الIR والintegrated thinking جوة الممارسات بتاعت الشركات عشان تمثل لها الnorm زي ما هنشوف

.

وعمل لنفسه vision تعمل align لتخصيص للcapital مع ال corporate behavior وكل ده عشان خاطر يوسع أهداف الfinancial

stability and sustainable development وده طبعا من خلال الcycle بتاعت الIR والintegrated thinking

.

وبعد اما حط الmission والvision قال يا جماعة وأنا هدفي بكل صراحة اني أغير نظام الcorporate reporting بحيث اخلي الIR يبقى global norm .

.

طبعا الاطار بتاع الIR ده زي ما قلنا قدم مفهوم التقرير عن الnon-financial information كجزء integral من التقرير السنوي بتاع الشركة اللي ربما يقرأ من كل الstakeholders.

.

وقبل ما نوريك ازاي هما وسعوا اوي مفهوم الstakeholders. هنقولك حاجة ظريفة اوي وان كان مستبعد انها تيجي في الامتحان

.

تلاحظ انهم اما جم بتوع ال Council بتاع الIIR يحط اختصار لكلمة الIR كان بيعرضها بsymbol شكله كدة <IR> عشان يختصر اسم الtopic ده بس اللي نفسنا نلفت انتباهك له ان:

.

The use of the less-than symbol and the greater-than symbol in the icon are noteworthy

.

طيب نمسك كلمة كلمة

.

اولا حتة الless-than

.

انهم بيقولوا يا جماعة :

.

The use of the less-than symbol is interesting

.

عشان خاطر الintegrated report ده لازم يكون concise, or short وزي ما بيقولوا يكون “to the point.”

.

فهما شايفين انهم في الحقيقة ان الاطار بتاعهم ده بيوضح ان الintegrated report بيعبر عن المفاهيم بشكل واضح وبكلمات قليلة.

.

“Expresses concepts clearly and in as few words as possible.”

.

وعليه:

As such, an integrated report is “less than” an entire annual report or 10-K.

.

دي ناحية .

.

من الناحية التانية عندنا ثانيا بقى حتة ال“greater than”

.

قالك مش ملاحظ ان التقرير ده جواه الsix capitals اللي هما الfinancial, manufactured, intellectual, human, social and relationship, and natural

.

يعني أهو الIR ده من الناحية دي اكبر من التقرير المالي السنوي التقليدي لان نطاقه زي ما انت شايف اوسع اهو.

.

As such, an integrated report is “greater than”

a traditional financially oriented annual report because it has a much broader scope.

.

يعني من الاخر نقدر نقول:

.

To summarize, <IR> is both “less than” and “greater than” traditional financial reporting

.

نرجع للكلام على توسعة مفهوم الstakeholders.

.

في الحقيقة:

Originally, an organization’s

stakeholders included those who could be expected to be significantly affected by the organization’s business

activities.

.

لكن في المقابل الIIRC وسع التعريف وكمان وسع الlist بتاعت المجموعات اللي هنعتبرها من الstakeholders.

.

فهتلاقيه وسع التعريف عشان يضم الناس اللي الactions بتاعتهم محتمل انها significantly affect the organization

.

وكمان وسع الlist

.

فجم قالوا:

.

[Stakeholders are] Those groups or individuals that can reasonably be expected to be significantly

affected by an organization’s business activities, outputs or outcomes,

.

(يعني مفعول به)

+

قالو:

or whose

actions can reasonably be expected to significantly affect the ability of the organization

to create value over time [emphasis added].

(يعني هما الفاعل نفسه)

.

وعليه نتصورهم في:

Stakeholders may include providers

of financial capital, employees, customers, suppliers, business partners, local communities,

NGOs, environmental groups, legislators, regulators, and policy-makers.

.

طيب احنا كدة في البوست ده عرضنا عنوان الThe International <IR> Framework من هوك.

>

نوقف البوست ده على كدة ونخش من البوست اللي جاي على

.

Integrated Report, Integrated Reporting, Integrated Thinking, and Their Relationships

نستعين بالله ونخش على عنوان

.

Integrated Report, Integrated Reporting, Integrated Thinking, and Their Relationships

.

وده هيبقى مهم جدًا عشان نبدأ نفهم أكتر المحاور الخاصة بالIR

.

طبعا زي ما حكينا ان الاطار بتاع الIR بنى مفاهيم الsocial responsibility and sustainable development لكن في الحقيقة هو بردو قدم لمفاهيم جديدة ومتطورة

.

طيب نمشى شوية مع التعريفات اللي قدمها الاطار بخصوص الintegrated report والIntegrated reporting والIntegrated thinking

.

بس احنا مش هنلطع تعريفات وخلاص على قدر ما احنا عايزين نفهم المقصود من وراها

.

الاطار عرف لنا الintegrated report والIntegrated reporting

.

طيب ما المتبادر للذهن ان الintegrated report ده هيبقى الادادة اللي بتمثل concise communication

.

بس التقرير ده بيدينا holistic view of the organization for all relevant stakeholders

.

وعلى الناحية التانية منطقيا الIntegrated reporting هيبقى الprocess اللي هطلع لنا الintegrated report ده بشكل دوري فيما يخص طبعا

الvalue creation over time اللي هو اصلا محور موضوعنا

.

يعني ببساطة عندنا تقرير هيطلع من خلال عملية الIntegrated reporting التقرير ده متوقع منه طبعا انه يورينا ازاي الاستراتيجية بتاعت الشركة ونظام حوكمتها وادائها هيضيف قيمة

بس طبعا في سياق الexternal environment

والمقصود هنا اننا نضمن حتة اضافة القيمة دي بس على مستوى short, medium, and long term

.

لاننا دايما بنقول In the context of the entity’s external environment

.

لان فيها الvalue is created عن طريق تقديم combination من الfinancial and nonfinancial information

.

بس خلي بالك ان الintegrated report ده مش

ere combination of the annual report with a separate

sustainability or corporate social responsibility report

.

لأ

ده لازم يبقى designated, identifiable communication.

.

****

.

اما العملية نفسها بتاعت الIntegrated reporting دي فهي ارتكزت اصلا على الIntegrated thinking والمقصود هنا بالIntegrated thinking

.

ان الشركة بتاعتنا يبقى تفكيرها Integrated يعني تاخد في الاعتبار (بس بشكل فعال) العلاقة بين الوحدات التشغيلية والوظيفية والcapitals اللي الشركة بتستخدمهم او بتأثر عليهم.

.

يعني مبنية على

connectivity and interdependencies among the organization-specific factors

.

اللي هتأثر على مقدرة الشركة على خلق قيمة على مدار الوقت.

.

.

طبعا الطريقة دي من ان الشركة تاخد في الاعتبار الكلام ده هيوصلنا ان حتة اتخاذ القرار تبقى بردو Integrated

وتوصلنا لحتة اضافة القيمة بردو على مستوى الover the short, medium, and long term.

.

****

فزي ما انت شايف ان الIntegrated Thinking يعتبر :

.

process of decision making, management, and reporting

.

.

طبعا الIntegrated thinking ده مفهوم مهم جدا في العملية بتاعت الIntegrated reporting دي

.

لانك لو خليت طريقة التفكير دي تبقى جوة كل انشطة الشركة الmanagement reporting بشكل طبيعي جدا

هيحط ويدخل الnon-financial information في الmanagement reporting وكمان في اي تحليلات او اتخاذ قرار.

.

وفي اللحظة دي الInformation systems بتاعت الشركات هتبقى Integrated بشكل افضل وهتبقى عنده قدرة افضل لدعم

الinternal and external reporting and communication

.

وعليه نقدر نقول ان الIntegrated thinking شرط ومتطلب اساسي للIR

.

وهنا جليم بيعلق وبيقول جملة ممتازة بيقولك

:

حتة فهم تأثير الfinancial and nonfinancial factors

مهم للاتي:

.

(1) report in an integrated manner

about the performance of the organization and

.

(2) make well-informed decisions for longterm

value creation.

.

.

Through integrated thinking, an organization learns how the interdependencies among

its financial and nonfinancial aspects interact and affect value creation. Thus, integrated

thinking is the basis for the externally communicated integrated report.

.

Integrated thinking cannot be done in a stand-alone department. Different departments must

work together to measure and report the value creation of the organization for both itself

and its environment.

.

طبعا تلاحظ ان الIR هيخلي شركتنا تحكي its own unique story of value creation

.

ويقدم لل

to give providers of financial capital

more information about how the entity creates value over a period of time.

.

وطبعا فوق الroviders of financial capital التقرير هيخدم ال

other stakeholders who are interested in the entity’s

effectiveness in creating value.

.

زي الemployees, customers, suppliers, communities in which the

entity is located, and assorted regulators.

أتمنى طبعا النظر للمفاهيم السابقة على اساس انها بinteract. مع بعضها

.

يعني يا جماعة بنقول والله الIR مش static concept لكن هو والله

.

process that continuously improves

reporting, internal decision making, and integrated thinking.

.

وزي ما قلنا ان الهدف الultimate للir انه يبقى corporate reporting norm سواء للpublic او حتى الprivate على مستوى العالم.

.

طيب نوقف البوست ده على كدة ونخش من البوستات اللي جاية على المفاهيم الخاصة بالCapitals” والغرض من ورا الIntegrated Reporting دخولا على الValue Creation

.

يسر الله الأمر وأعان.